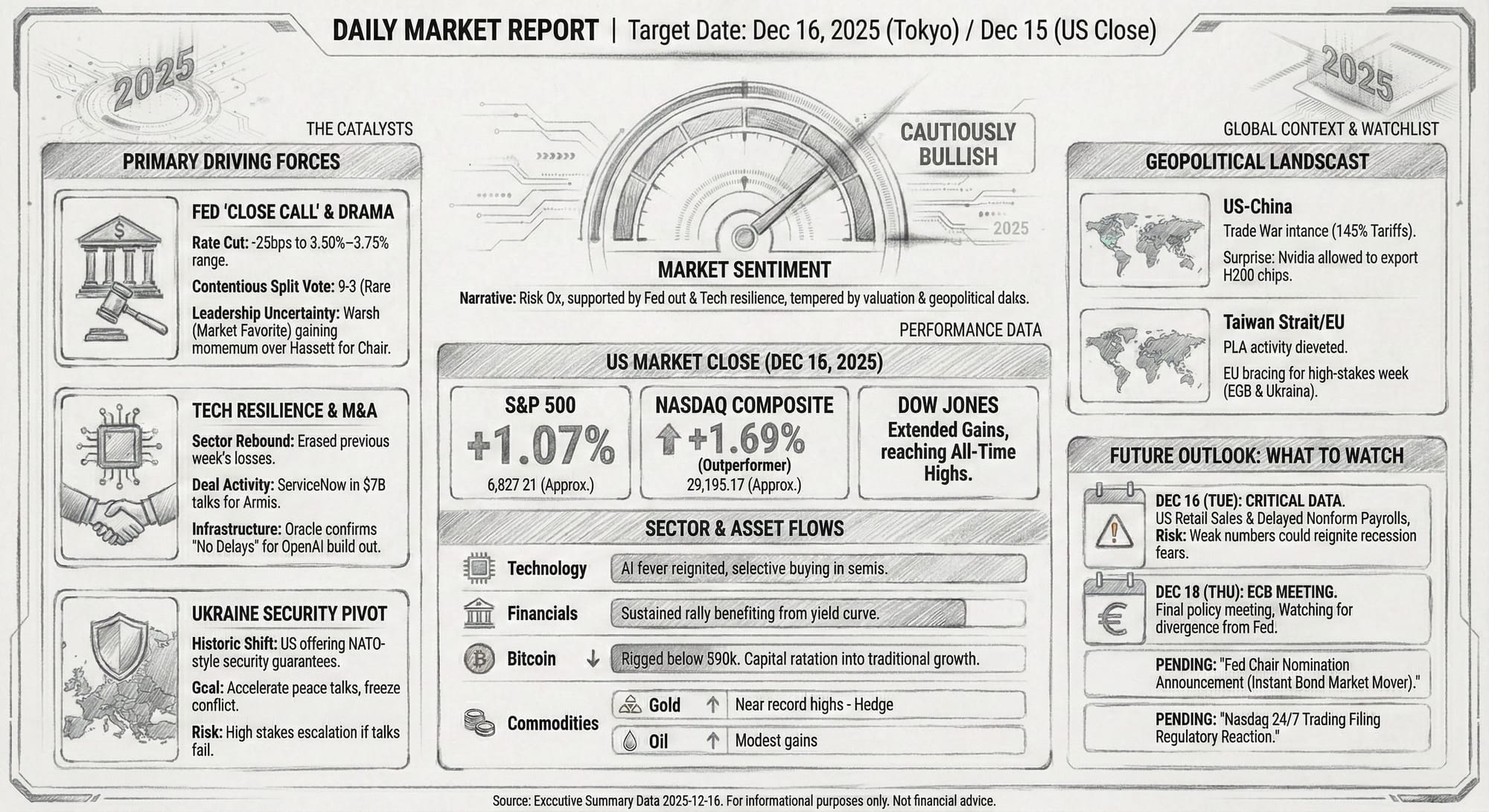

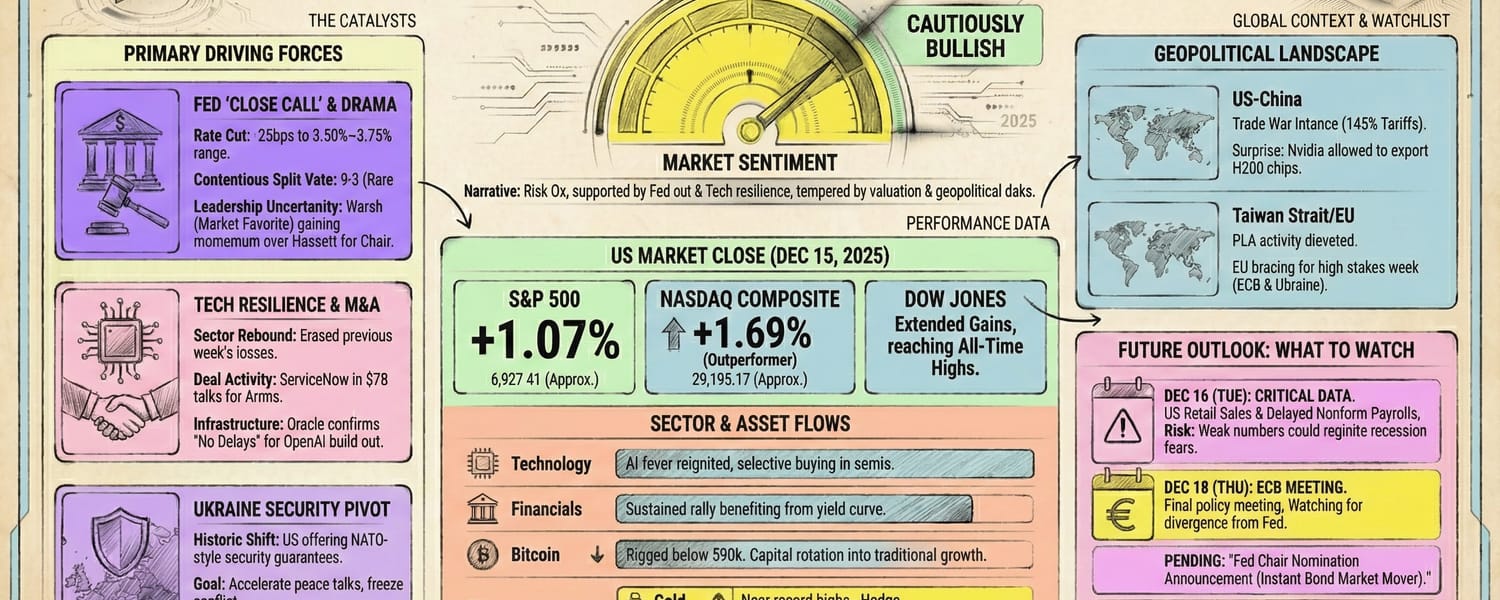

Target Date: December 16, 2025 (Tokyo Time) / December 15, 2025 (US Close)

Executive Summary

Global markets entered the Asian trading session of December 16, 2025, on a strong footing, following a robust performance in the United States where major indices rebounded significantly. The S&P 500 and Nasdaq Composite posted gains of over 1% and 1.6% respectively on December 15, erasing losses from the previous week's volatility. Market sentiment is currently defined by a "cautiously bullish" narrative: investors are celebrating the Federal Reserve's recent rate cut—despite it being a contentious "close call"—while keeping a wary eye on potential bubbles in the Artificial Intelligence sector.

The driving forces behind today's market moves are threefold. First, the digest of the Federal Reserve’s split decision to cut rates to the 3.50%–3.75% range has stabilized bond yields, although political maneuvering regarding the next Fed Chair is injecting uncertainty. Second, the technology sector is seeing renewed M&A activity, notably ServiceNow’s reported $7 billion acquisition talks, which has helped calm fears of an AI spending slowdown. Third, major geopolitical shifts are underway, with the US reportedly offering NATO-style security guarantees to Ukraine, a move that could accelerate peace talks but heighten tensions with Moscow.

Key Events Analysis: Top 3 Critical Developments

1. The Federal Reserve's "Close Call" & Leadership Drama

The aftershocks of the Federal Open Market Committee (FOMC) meeting continue to reverberate through global asset classes. On December 10, the Fed lowered the federal funds rate by 25 basis points to a target range of 3.50%–3.75%. However, the decision was far from unanimous, resulting in a rare 9-3 vote split. This dissent—with one member pushing for a deeper 50 basis point cut and two arguing for no change—signals deep uncertainty within the central bank regarding the path of inflation versus labor market risks.

Compounding this monetary policy uncertainty is the political intrigue surrounding the Federal Reserve Chairmanship. Reports indicate that President Donald Trump is reconsidering his support for Kevin Hassett due to market concerns over his perceived lack of independence. Momentum has shifted toward former Fed Governor Kevin Warsh, favored by Wall Street heavyweights like Jamie Dimon. Prediction markets have reacted swiftly, slashing odds for Hassett and boosting Warsh. This political tussle is critical for investors; a Chair perceived as too pliable to the White House could unanchor inflation expectations and spike long-term bond yields, countering the benefits of recent rate cuts.

2. Tech Sector Resilience & Major M&A Activity

Following a sharp sell-off on December 12 driven by "AI bubble" fears, the technology sector staged a convincing rebound on December 15. A key catalyst was the report that ServiceNow is in advanced talks to acquire cybersecurity firm Armis for approximately $7 billion. This deal signals that despite high valuations, software and enterprise tech companies remain aggressively in expansion mode, validating the "growth" narrative.

Furthermore, Oracle helped stabilize sentiment by formally refuting Bloomberg reports claiming delays in its massive data center build-out for OpenAI. By stating unequivocally that there are "no delays," Oracle alleviated fears of an infrastructure bottleneck that could have derailed the broader AI hardware rally. However, volatility remains; broadly, the market is rotating. While tech led the rebound today, there is a distinct broadening of the rally into financials and banks, which are benefitting from the steepening yield curve.

3. Ukraine Security Guarantees & Geopolitical Pivot

A potentially historic shift in the Russia-Ukraine war is emerging. US officials have indicated that Ukraine could receive security guarantees modeled on NATO’s Article 5 mutual defense pledge as part of a proposed peace deal. This is an unprecedented offer intended to bring Russia to the negotiating table and freeze the conflict, nearly four years after the full-scale invasion.

For markets, this development is a double-edged sword. On one hand, a credible path to a ceasefire removes a massive overhang of geopolitical risk and could stabilize European energy and commodity markets. On the other, such a guarantee significantly raises the stakes for US involvement, potentially escalating tensions if the ceasefire fails. This news has already influenced commodity markets, with gold prices pushing near record highs as a hedge against the complex geopolitical realignment, while oil prices have seen modest gains.

Market Performance: US Stocks & Tech

US Market Close (December 15, 2025): The US equity markets closed firmly in positive territory, setting a bullish tone for the Asian session. * S&P 500: Closed up 1.07% at approximately 6,827.41. * Nasdaq Composite: Outperformed, rising 1.69% to finish around 23,195.17. * Dow Jones Industrial Average: Extended recent gains, contributing to the all-time highs seen across indices.

Sector Performance: * Technology: The primary driver of the day's gains. The "AI fever," which cooled late last week, reignited with selective buying. Investors bought the dip in semiconductor stocks, shrugging off Broadcom’s recent volatility. * Financials: Bank stocks are enjoying a sustained rally, poised for their third consecutive week of gains. The rate environment—lower short-term rates but stable long-term growth prospects—is proving ideal for net interest margins. * Cryptocurrency: Bitcoin trended lower, dipping below the psychological $90,000 threshold despite the risk-on sentiment in equities. This divergence suggests capital rotation out of digital assets into traditional growth equities.

Significant Company News: * ServiceNow: In focus due to the $7 billion potential acquisition of Armis. * Oracle: Shares remained active as the company fought back against negative press regarding OpenAI infrastructure delays. * Nasdaq: The exchange is planning to file paperwork with the SEC to launch round-the-clock (24/7) trading for stocks, a move that could fundamentally alter global liquidity dynamics.

Geopolitical Update

- US-China Relations: The trade war remains intense with the US maintaining a 145% tariff on Chinese goods. However, a surprising nuance has emerged: The US administration has permitted Nvidia to export advanced H200 semiconductors to China. This decision, seemingly contradictory to the "tech containment" strategy, may be a bargaining chip in broader trade negotiations but risks narrowing the AI capabilities gap between the two superpowers.

- Taiwan Strait: Tensions remain elevated. The PLA has increased military activities around Japan and Taiwan, including radar lock-ons. Taiwan is considering restarting decommissioned nuclear plants to secure energy independence in the event of a blockade.

- European Union: Europe is bracing for a high-stakes week. Beyond the Ukraine peace talks, the European Central Bank (ECB) is preparing for its final policy meeting of the year, with markets expecting growth forecasts to be lifted.

Future Outlook

Market Sentiment: The immediate sentiment is Risk-On, but fragile. The market is pricing in a "Goldilocks" scenario: falling inflation, supportive Fed policy, and resilient AI growth. However, the dissent within the Fed and the high valuation of tech stocks leave little room for error.

What to Watch (Tomorrow & Next Week): 1. Economic Data Releases: Tuesday (Dec 16) is a critical data day. Watch for US Retail Sales and Nonfarm Payrolls (delayed release). Weak numbers could reignite recession fears that the Fed's cut arrived too late. 2. ECB Policy Meeting (Thursday): With US rates heading down, global investors will look to the ECB to see if they follow suit or hold steady. A divergence in policy could spark volatility in the EUR/USD currency pair. 3. Fed Chair Nomination: Any official announcement regarding the nomination of Kevin Warsh or Kevin Hassett will move bond markets instantly. A Warsh nomination would likely be viewed as "market-friendly" and supportive of Fed independence. 4. Nasdaq 24/7 Trading Filing: Monitor regulatory reactions to Nasdaq's proposal for round-the-clock trading. If approved, this would signal a major structural shift for 2026.